Image Source: Getty Images

ISA stocks and stocks are exceptional ways to generate passive income. As tax benefits increase capital gains and dividend income, lump sum or regular investments can provide life-changing secondary income upon retirement.

If investors park £20,000 in one of today’s ISAs, there is a way they can ultimately enjoy tax-free cash payments of around £1,000 each month.

Please note that tax procedures depend on each client’s individual circumstances and may change in the future. The content in this article is for informational purposes only. It is not a form of tax advice or constitutes. Readers are responsible for carrying out their own due diligence and obtaining professional advice before making investment decisions.

Target £1k

There are multiple ways that individuals can target passive income when they retire.

You can either lower your setting rate from your portfolio or switch to dividend stocks that pay regular income. You can also purchase annuities that offer a lifetime guaranteed amount. Alternatively, you can choose some or all of the above combinations.

I like the idea of buying dividend stocks. Over time, you can earn a second income while ensuring the range of growth in your portfolio. That’s the road I’m planning to get off. So, how big should my ISA be for a monthly salary of around £1,000?

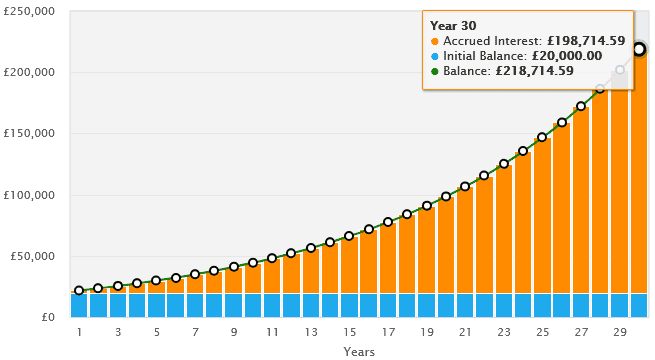

If you target dividend stocks at a 6% yield, you will need to sit at £218,715 in your portfolio when you retire. It would offer me £1,094 a month.

To achieve this at £20,000 in my ISA, I have to target an average annual return rate of 8% over 30 years.

But how realistic is this kind of return? If the long-term performance of the stock market is fine, “very” is the answer.

Robust returns

| Stock Market Index | 10-year average annual revenue |

|---|---|

| FTSE 100 | 6% |

| S&P 500 | 11.7% |

| average | 8.9% |

As you can see, those who invested in UK and US blue chip stocks would have enjoyed an average profit of almost 9% over the past decade.

History is not always a reliable guide to future investment returns. But the broader stock market has proven its ability to rebound from the crisis and deliver strong profits over time.

Investors today can target large incomes by investing in individual stocks and purchasing Exchange Transaction Funds (ETFs). iShares S&P 500 ETF For example, (LSE:CSPX) is worth considering as a direct way to take advantage of the great long-term returns of the S&P 500.

This is the fund I own in my portfolio. By spreading cash to hundreds of US stocks, you can capture the great growth potential of high-tech stocks ( nvidia and apple) While diversifying to reduce risk.

A third (31.6%) of the funds are dedicated to information technology companies. The rest spreads across multiple sectors, including financial services, consumer goods, telecommunications and healthcare.

By reinvesting dividends, this fund is overcoming long-term growth using the power of compound interest to earn profits on all my past returns.

Such funds can produce poor returns during recessions. But over time, they were a great way to unlock healthy income for retirement.